In most state Marketplaces (Exchanges)*, consumers can choose pediatric dental coverage as part of their medical policy or as a separate dental policy. Pediatric dental coverage is defined as dental benefits for anyone through age 18. Children's dental health is your choice as part of the essential benefits offered on Exchanges and in the small employer group (consisting of 50 or fewer full-time employees) and individual market outside of Exchanges. What you choose comes down to what you know. Here are 5 tips to make your choice a wise one.

Key takeaways:

- Determine if the Dentist You Use is on the Network

- Check How the Deductible is Applied to Your Benefits

- Understand the Impact of the Consumer Out-of-Pocket Maximum

- Examine the Definition of Medically Necessary Orthodontia

- Know When Pediatric Dental Premium is Eligible for a Subsidy

Determine if the Dentist You Use is on the Network

Consumer surveys show that eight in ten consumers have a dentist or a dental practice they normally use for dental care. Nationwide, roughly 87% of practicing dentists participate in dental PPOs, but this varies from state to state and carrier to carrier. Medical plans generally do not have dental networks but may have a dental affiliate or a contract with a stand-alone dental plan to use their network to support the pediatric dental benefit they offer. If keeping your dentist is an important factor in selecting pediatric dental benefits, check whether your dentist is in the network first.

Check How the Deductible is Applied to Your Benefits

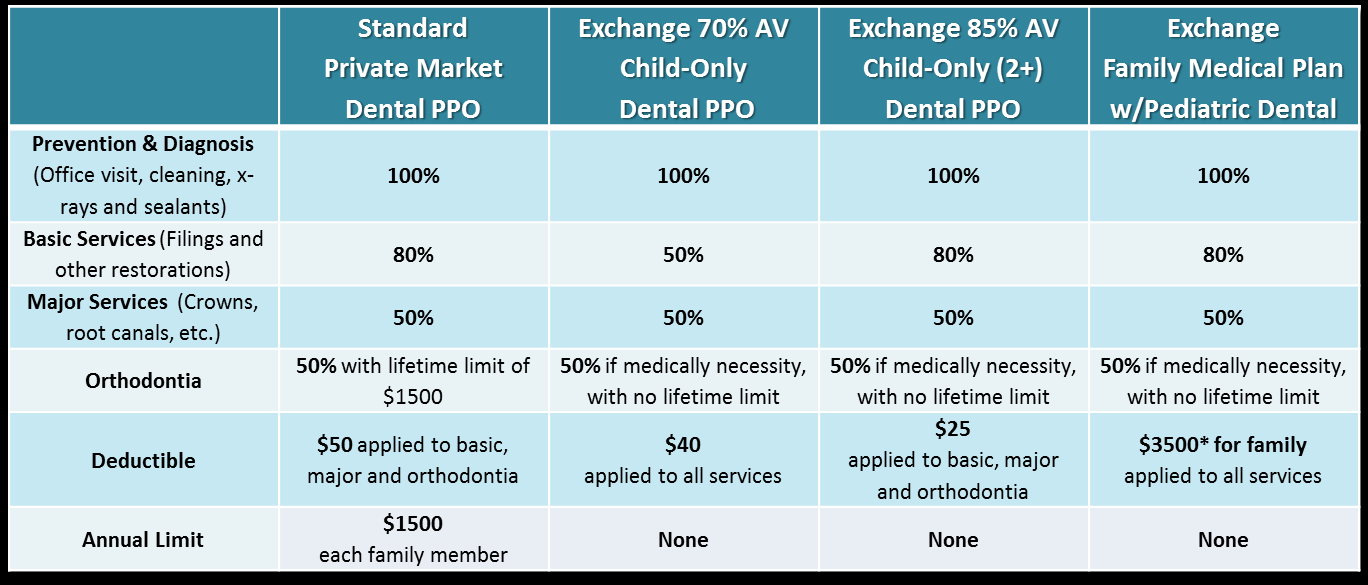

When considering whether to buy your child’s dental benefits as part of a medical policy or in a separate policy, be sure you look at the details to determine the coverage you are getting. The policies illustrated in the chart below** all provide benefits for pediatric dental. While the policies look similar based on the percentages paid by the insurer for dental procedures, these policies result in very different out-of-pocket costs for you and your family because of the deductible.

The most critical factor to examine when evaluating policy options is how the deductible is applied.

If it is applied to all services under a medical policy, you can pay most and sometimes all of your children’s typical dental expenses out of pocket—unless your family has significant medical expenses. Separate dental policies usually have deductibles of less than $100 and the deductible is often not applied to prevention and diagnosis so that your periodic office visits, cleanings, x-rays, and sealants cost you nothing.

NADP Executive Director Evelyn Ireland explained, “Today only 30% to 40% of consumers with medical policies meet their annual medical deductible. If you are in the 60% to 70% that don’t, you could be paying most, if not all, of your children’s dental costs out of your pocket when a medical plan makes children’s dental subject to the medical deductible. This is the most critical factor for consumers to examine when pediatric dental is included in a medical policy. The increase in medical policy premium for your child’s dental may be small, but out-of-pocket costs for treatment may also be higher than in a stand-alone dental policy. In a stand-alone dental policy, premiums may be greater than the difference between a medical plan without pediatric dental benefits and one with pediatric dental benefits, but out-of-pocket costs will typically be lower. Consumers should weigh premium impact against out-of-pocket costs to ensure they are getting the benefit they expect. ”

*Medical deductibles can be up to $2000 for one person covered under a policy or $4000 when more than one person is covered under the policy. $1500 to $3500 is a common range for Exchange policies.

Understand the Impact of the Consumer Out-of-Pocket Maximum

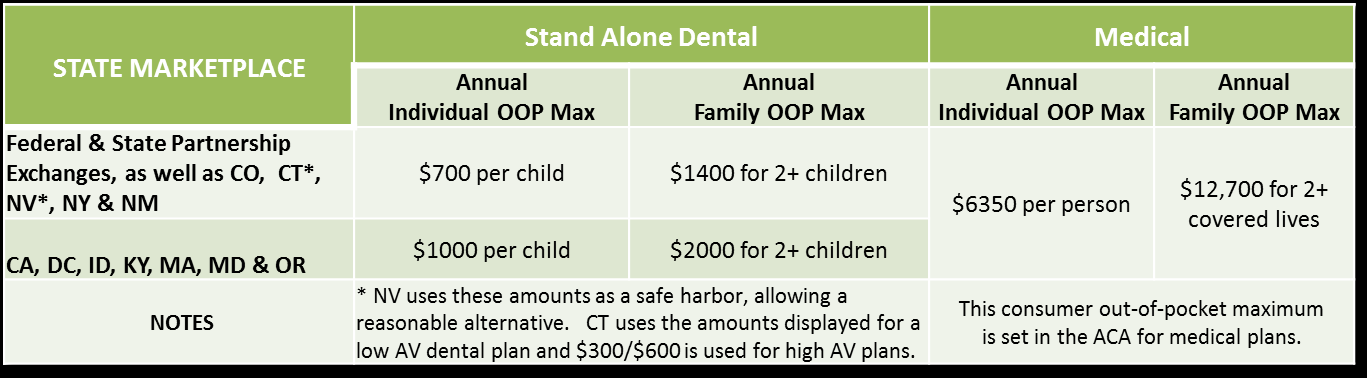

The consumer out-of-pocket maximum is the most you have to pay out of your pocket during the year for covered services when you use a dentist that is in your plan’s network. It is basically what your deductible, co-insurance, and co-payments add up to during the year. The maximum annual OOP for pediatric dental is $700 for one child and $1400 for two or more children in a family in most states (see chart for variations); for medical it is $6350 for an individual and $12700 for a family.

When you reach these limits, the carrier pays 100% of the covered dental or medical care for the rest of the year. But the limits are different for medical and separate dental policies creating differences in what you will pay out-of-pocket when high-cost procedures like crowns or orthodontia are needed. Below is an example of how the limits may apply to a child with orthodontic needs.

- CONSUMER OOP MAXIMUM EXAMPLE: The average national cost of orthodontia is $6350 and treatment is most often spread over two years. Orthodontic costs are usually split with the consumer and the insurer each paying 50% (see above chart) after the deductible. If your child qualifies for medically necessary orthodontia, in the first year treatment costs could be $3000. Here is how the cost-sharing would work under a separate dental plan and a medical plan:

- Separate Dental: In the case of a stand-alone dental plan in Texas (an FFM state), let’s use the Exchange 85% AV Child-Only Dental PPO from the previous chart. Assume the child has had no services other than a preventive visit where the diagnosis was for orthodontia. The consumer would pay the deductible of$25 after which the dental plan and consumer split the costs 50%/50% until the consumer reaches the OOP limit of $700. So the consumer pays $700 (see the chart of OOP limits below) and the insurer pays $675 (matching the payment made after the deductible)—together these payment total $1375. The $1625 that is left for the annual cost of orthodontic treatment is paid 100% by the dental plan.

**Total consumer out of pocket payment = $700; total dental plan payment = $2300.

Medical with Dental: In the case of a medical plan covering pediatric dental, there could be several scenarios:

- The insurer and consumer each would pay $1500 IF the consumer had already reached their medical deductible or a small deductible was applied to dental; or

- if the deductible was $3500 (see previous chart) and the family had only paid $1000 of the deductible before orthodontic care was needed, the family would pay the first $2500 of orthodontic treatment as the remainder of the deductible and the insurer and family would split the remaining $500; or

- if none of the deductibles had been met, the consumer would pay the full $3000 cost of orthodontia this year;

> Total consumer out-of-pocket payment ranges from $1500 to $3000; medical plan payments range from $0 to $1500.

Ms. Ireland explains, “Actuarial studies show that only 7% to 12% of consumers hit a medical out-of-pocket maximum annually. So, the consumer medical cap on out-of-pocket expenses never comes into play for about 90% of consumers. While there is no experience in the marketplace with a dental consumer out-of-pocket maximum, industry data suggests that only 2% of claims for children will hit the dental out-of-pocket maximum—primarily for medically necessary orthodontia. This means that the deductible is the major factor in consumer out-of-pocket costs under a medical policy, not the out-of-pocket maximum. And under a dental policy for most consumers, the co-insurance or co-payment amounts are the major factor. The out-of-pocket maximum comes into play under a separate dental policy primarily for medically necessary orthodontia or when a child has significant dental needs. Under a medical policy, the out-of-pocket maximum would only come into play when the child with significant dental needs was in the 10% of families that hit their medical out-of-pocket maximum.”

Stand-alone dental is required by rule to have a "reasonable" consumer out of pocket. States & the FFM have defined "reasonable" for 2014 as amounts shown.

Examine the Definition of Medically Necessary Orthodontia

When orthodontia is covered as part of the pediatric dental benefit defined by a state (all states but Michigan, and Utah), federal rules limit the coverage to “medically necessary” orthodontia. When medical necessity is not defined, HHS FAQs make each insurer—medical and dental - responsible for defining medical necessity in their policies. Orthodontia may be limited to severe deformities or defined by a clinical scale that your dentist must use to measure your child’s needs. Depending on the definition, NADP estimates that about one-third of the children that have orthodontic procedures each year will qualify under the varied definitions of medically necessary orthodontia5. Consumers should check the definition of medically necessary orthodontia in policies they are considering if they anticipate that these services may be needed by a family member.

Know When Pediatric Dental Premium is Eligible for a Subsidy

You can get a subsidy for the pediatric dental premium when you buy coverage in Exchange. Subsidies are only available through state or federal exchanges. When you buy a bronze medical policy on an Exchange, the premium of a separate dental policy for your children is added to your medical policy to calculate your total subsidy. When you buy a medical plan that includes dental benefits for your children, you are also getting a subsidy for dental.

Sometimes a subsidy is not available. If you buy a silver or higher-value medical policy, the amount of your subsidy is based on the 2nd lowest-cost silver plan that you could buy in your state. This is called a benchmark plan. If the benchmark plan does not include pediatric dental, the premium for your children’s dental benefits is not included in your subsidy. This benchmark plan applies whether you purchase a medical policy with pediatric dental benefits included or a stand-alone dental policy covering your children.

This could change before you have to file your taxes for 2015 as dentists, consumers, dental insurers and 14 US Senators have asked IRS to fix this so that all consumers that are purchasing dental benefits for their children through an Exchange have the cost of pediatric dental included when they qualify for a subsidy.

BONUS TIP: Adult Dental Can also be Purchased on Exchanges

In most Exchanges, you can combine the new dental coverage for your children with dental coverage for you and your family. The special rules described above do not apply to adult coverage under a family policy.

Content is courtesy of the National Association of Dental Plans, of which Solstice is a member.

Want to have Solstice benefits?

Call our sales team at 877.760.2247 or email Sales@SolsticeBenefits.com

Already have Solstice benefits?

See your plan details by going to https://www.mysmile365.com/ or calling us at 1.877.760.2247.

comments