Insurance is well-known for its use of acronyms, benefit terminology and health care jargon. From SADPs to actuarial values to the MOOP, it’s hard to keep track of the terms that comprise the Affordable Care Act (ACA).

We’re in the industry and understand the confusion around many of these terms. Understandably, your clients must have even more questions about the information relating to healthcare rights and reform, and how it impacts their organization and their employees.

If you need and your clients need help deciphering the ACA alphabet soup, we’ve compiled the top list of ACA terms and acronyms to help brokers, employers, and consumers.

- EHB: The ACA requires insurance companies to offer certain essential health benefits or “EHBs.” EHBs are 10 categories of health services that the legislation deems essential. They include such services as pediatric dental care, maternity and newborn care, and preventive and wellness services.

- MOOP: The ACA imposes an annual limit on cost sharing, commonly referred to as a Maximum Out-of-Pocket, or MOOP. The acronym sounds funny, but it’s important. Here’s some other information for reference: The MOOP on a dental plan in 2020 was $350 for one (1) child, and $700 for more than one (1) child.

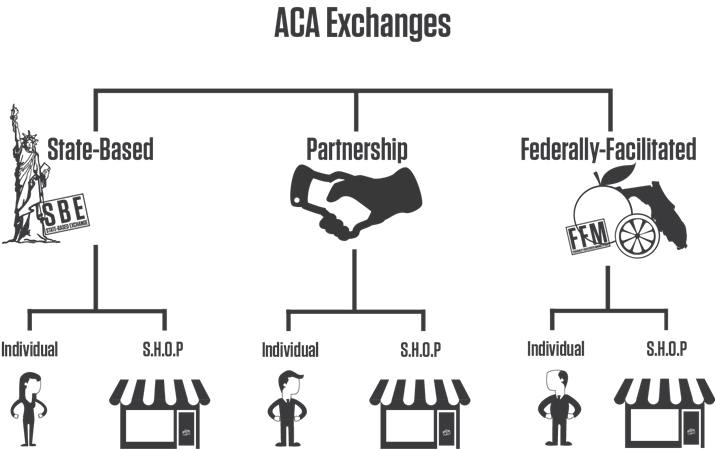

- SHOP: When small businesses (50 or fewer) offer insurance to their employees, one method of obtaining coverage is through the Small Business Health Options Program or SHOP. This is a separate portion of the federal and state exchanges where employer groups can purchase plans for their employees. Depending on the exchange, when an employer offers SHOP products to their employees, they will have the opportunity to select from any carrier offering a QHP or QDP in that state’s exchange (more on those later). Unlike traditional group benefits, the employee has the flexibility to choose any carrier and any plan that best fits their unique needs. Employer groups can use healthcare.gov to browse and compare plans, but will have to work with an agent, broker, or insurance company to enroll…great news for you, their broker!

- SADP: Stand Alone Dental Plan. Simply put, this is a dental plan that is offered without being bundled with or embedded into a medical plan.

- QDP: Qualified Dental Plan. These are dental plans approved by CMS or the state for sale on federal or state exchanges. In 2014, these plans are offered in two categories: high and low.

- QHP: Qualified Health Plan. Just like QDPs, these are medical plans approved by CMS or states for sale on federal or state exchanges. But unlike QDPs, these are offered and categorized by four "Meta Levels." It’s important to note that QDPs and QHPs can be offered for sale outside of the exchanges as well. This means that you might see these same qualified plans offered on carrier websites and private exchanges. Brokers can also sell these products to their SHOP and individual consumers.

- Metal Levels: One of the main ways the ACA is creating standardization of benefits is by segmenting QHPs into four metal levels: bronze, silver, gold, and platinum. This allows for apples-to-apples comparisons when individuals and employers go to the ACA exchanges to buy insurance. It's designed to help make coverage decisions much easier. The metal level of each plan tells you what percentage of cost you can expect the plan to cover. For example, a silver plan will, on average, cover 70 percent of all costs, leaving you to pay about 30 percent. A bronze plan will be less rich, and cover about 60 percent of all benefit costs, while a Platinum Plan will be the richest and cover about 90 percent of the costs. Meanwhile, QDPs have different benefit levels called either “high” or “low.” On the low plan you have will coverage of about 70 percent of all costs, while a high plan will cover about 85 percent.

Now, how do SADPs, QDPs, QHPs and Metal Levels work together?

In the pre-ACA world, people may have had difficulty comparing health plans, because of different benefits and out-of-pocket costs. The ACA sought to address this by requiring insurance companies to standardize the types of benefits and cost sharing in their plans. These standardized plans are QDPs and QHPs and are certified as such before they’re offered for sale on an ACA exchange. No plan gets on an ACA exchange without this stamp of approval.

Here’s what the ACA exchanges look for prior to giving their stamp of approval:

First, the plans have to offer EHBs. EHBs assure plans offered in the ACA Exchanges provide a baseline of coverage. One EHB you should be familiar with is the pediatric dental EHB.

Next, the plans must meet specific cost-sharing requirements. Cost sharing refers to the amount an enrollee has to pay out-of-pocket for covered services. The term generally includes deductibles, coinsurance and copayments, or similar charges.

ACA Exchanges: Health Insurance Marketplaces, or HIX, are also known simply as Exchanges. Each state provides access to a HIX. Each HIX is either a Federally Facilitated Marketplace (FFM) or a State-Based Exchange (SBE). Florida, for instance, uses the FFM HIX. New York has its own HIX called the New York State of Health. Both are government run and adhere to strict regulations and requirements mandated by the ACA. Individuals and small groups can purchase health insurance through these HIX. Since 2014, the number of people enrolled in benefits via a HIX has increased each year from over 8 million to more than 14 million.

It’s important to note that private exchanges and marketplaces are not ACA-mandated. Private exchanges are typically backed by an independent organization or carrier and not affiliated with any governmental agency.

Navigators: Consumers enrolling in benefits through public exchanges will likely have questions. This is where navigators come in. Navigators are available to assist HIX shoppers with benefit selection and help answer their questions relating to the plans and the exchanges. Navigators must be certified to participate. Navigators don’t necessarily need to be licensed insurance agents, but they cannot be employed by a carrier or receive incentives from a carrier.

APTC: Advanced Premium Tax Credits are available only through ACA exchanges and are not available to everyone. APTCs help make insurance more affordable for individuals with household incomes between 100 percent and 400 percent of the Federal Poverty Guidelines by lowering premiums.

When people enroll in health plans through an ACA exchange, they may be able to reduce their health plan premiums right away. Unlike with most tax credits, consumers won’t have to wait until tax time to get them. People who qualify can take their APTC right away in the form of an advance payment to lower their monthly premium. You will know the amount of the tax credit right after completing your application. The amount of tax credit depends on how much income a consumer’s family expects to earn. That’s why it’s important to fill out your application accurately. If the amount of income reported isn’t accurate, the consumer may not get the right amount of tax credit, or worse, the consumer could have to pay back money at the end of the year.

Certain small employers – those with fewer than 25 full-time employees (FTEs) – will also be able to get help with their costs. This is called the Small Employer Tax Credit.

Whew! You’re now up to speed on some of the most frequently used ACA terms. These will surely help you in your daily business as you help guide your clients through reform and into medical and dental plans to fit their needs.

Any questions about your current Solstice products? Login to your portal on https://www.solsticemarketplace.com/

Want to start selling Solstice? Give us a call at 877-760-2247 or email us at sales@solsticebenefits.com

comments